INFOGRAPHIC: How Fortnite, Roblox, and GTA V Locked Down the U.S. Market

New market data released by the ESA and Circana on February 11 shows U.S. video game spending reached $60.7 billion in 2025, up 1.4% year-on-year, with $62.8 billion projected for 2026.

That growth is not being distributed across a widening slate of titles. It is being captured by a shrinking group of ecosystems that have held the top of the market for two consecutive years without giving ground. Fortnite, Roblox, and GTA V are not just the most-played games in the U.S., they are the reason the market looks the way it does. The top five most-played games on U.S. PlayStation 5 in 2025 were the same five titles, in the same order, as 2024. On Xbox, the same names are held with only marginal rank shifts. The market is growing, but it is growing inside walls that were already built.

"What the data confirms is that U.S. gamers are not browsing, they are returning," says Alex Zhou, Senior Gaming Industry Analyst at LDShop. "Fortnite, Roblox, and GTA have stopped competing for attention on a level playing field. They have become the default, and defaults are very hard to displace."

The Numbers That Show the Lock

Data confirms where attention has gone:

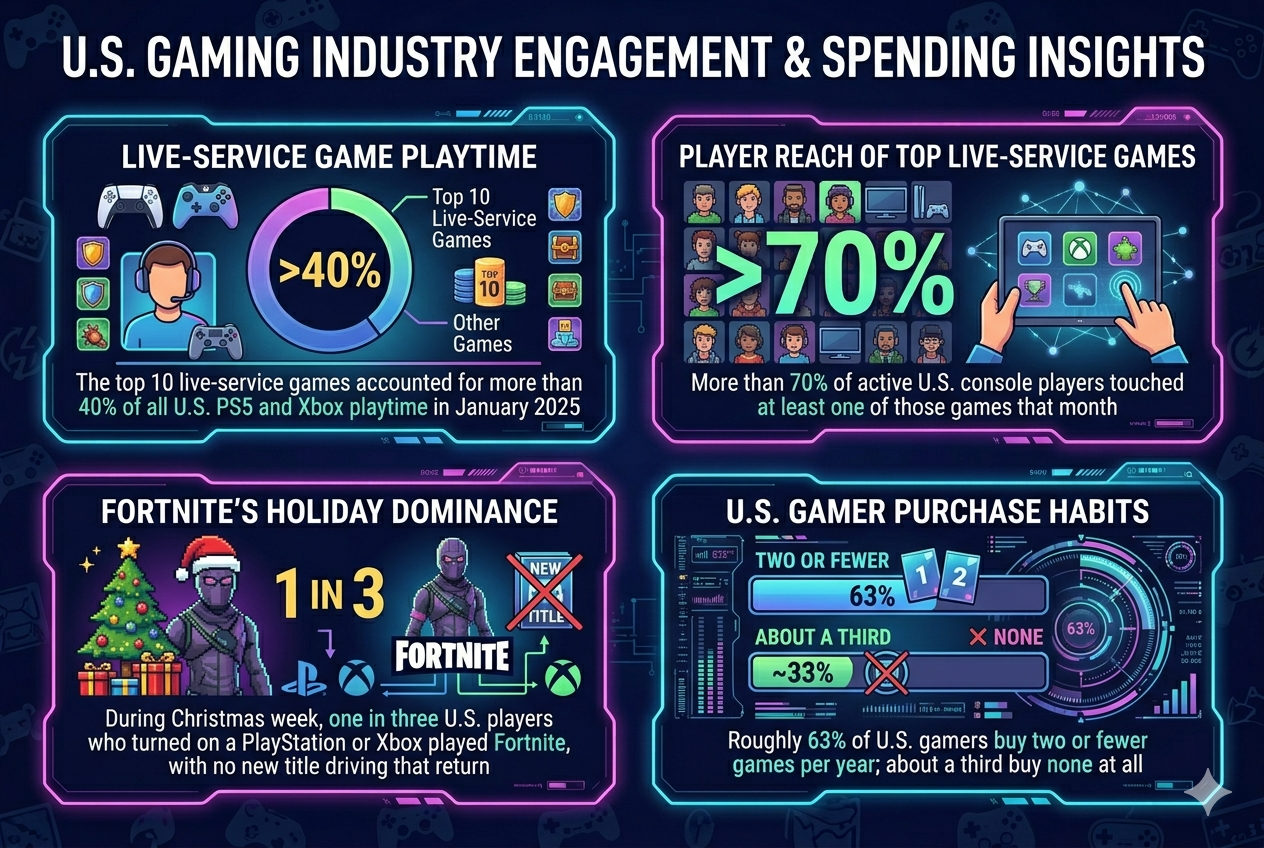

More than 205 million Americans play video games. But their time is not spreading across new releases. It is pooling inside a fixed group of platforms that have already earned their place in weekly habits.

Three Games, Three Versions, Same Outcome

Fortnite, Roblox, and GTA are not running the same model. They have arrived at the same result through different mechanisms.

Fortnite runs on gravity. One in three U.S. console users defaulted to it during the year's highest-traffic gaming week. That is not novelty, but a habit so deeply embedded that free time automatically routes back to the same destination.

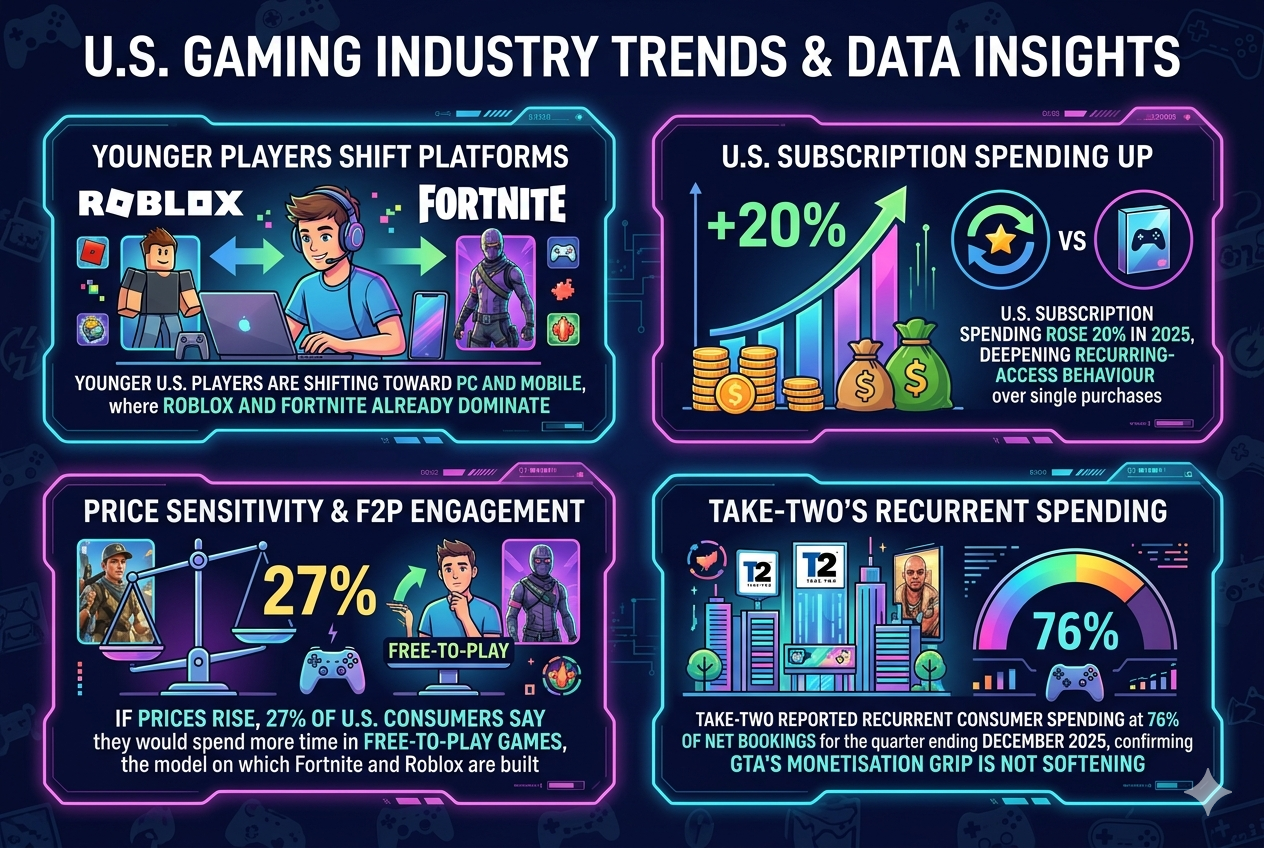

Roblox runs on platform behaviour. In Q4 2025, U.S. and Canada DAUs grew 32% year-on-year, while hours grew 41%, neither figure tied to a single launch. Users are not returning to play a specific game. They are returning to a place. "Year after year after year, we are seeing 20% growth," says Matthew Ball, analyst and author of The Game Business. "Its size, its regularity of growth, and the size of its growth, it's hard for me to say I'm not a believer in it as an important growth engine for the industry."

GTA runs on recurring spend. Take-Two reported recurrent consumer spending at 80% of FY2025 net bookings, with GTA Online among the largest contributors. A game released in 2013 is generating its strongest monetisation numbers more than a decade later. Circana analyst Mat Piscatella put it plainly: "Grand Theft Auto 5 launched in 2013, and it's still one of the top 20 best-selling games every single month. The biggest competitor to Grand Theft Auto 6 will be Grand Theft Auto 5."

Why the Advantage Compounds

The conditions reinforcing these ecosystems are getting stronger, not weaker:

That $62.8 billion projection for 2026 is real. But the data makes clear where it is flowing, into ecosystems already entrenched, not into new ones forming at the edges.

The Actual Competition

The question for U.S. gaming is no longer which new title launches next. It is whether any new title can compete with platforms that have already captured the player's time, habit, and wallet, and are building conditions that make that hold tighter every year.

About LDShop: LDShop is a global game top-up platform, offering players discounted in-game currency, gift cards, and recharge services across hundreds of popular titles, including Genshin Impact, PUBG Mobile, and Fortnite. Trusted by gamers worldwide, LDShop provides fast, secure transactions and localized customer support across multiple languages.

Sources

Circana Forecasts a Transformative Year for Video Games in 2026

2025's Top 5 Most-Played Games On PlayStation And Xbox Are The Same As 2024's In The US - GameSpot

Majority Of US Gamers Buy A Max Of Two Games Annually, Analysts Say - GameSpot

Archive of the Annual Essential Facts About the U.S. Video Game Industry Report

My chat with Matthew Ball on what might turn the video game industry around

Take-Two Interactive Software, Inc. Reports Results for Fourth Quarter and Fiscal Year 2025

GTA 6's biggest competitor is GTA 5, not other new games, analyst says

Take-Two Interactive Software, Inc. Reports Results for Fiscal Third Quarter 2026